401(k) Investment Menu; Less is More

There was a time in the 401(k) business when more fund choices seemed like the best way to give participants what they want. This approach eventually led to too many plans offering confusing and overlapping fund choices in their 401(k) plans. This didn’t help participants, just confused them.

In this article “Constructing an Investment Menu for a Participant Directed Retirement Plan”. Joseph Topp of Francis Investment Counsel LLC provides some excellent guidance on how to build an investment menu that will be both attractive and effective for any retirement plan.

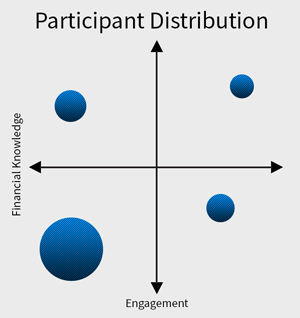

A key issue in developing an appropriate investment menu is that any plan with more than 100 participants there will be distinct segments along two key axes; financial knowledge and financial interest/engagement. We can plot it like this:

The way we used to build menus in 401(k) plans depended on providing lots of investment options and then “educating” participants about long-term investing principles. This is an effective approach for high knowledge, high engagement participants, but a spectacular failure for everyone else. I don’t have any studies at hand, but based on our own participant universe I’d estimate that no more than 15% of plan participants meet those criteria. What are we to do for the rest?

This is where Mr. Topp’s article shares two concepts that plan sponsors need to keep in mind when constructing investment menus. Behavioral Finance matters here. There are two common mistakes people make in 401(k) investment allocation. One is called “naïve diversification” where participants spread their money evenly across all funds and the other is “home bias” where participants over-invest in US based equities and bonds. The composition of the menu can have a dramatic impact on how costly these two mistakes are.

The second key development has been the (now ubiquitous) trend of including age/risk based portfolios (TDFs, Model Portfolios) that participants can choose depending on their particular life situation. In this case, all they have to do is figure out how long they plan to work and roughly assess their risk tolerance. With these two questions answered, they can then invest in a sophisticated fund designed for optimal long-term risk-adjusted return.

So where does that leave us? Best case scenario is a set of (10 to 12) high-quality, low-cost core funds representing the most important domestic and international asset classes plus a set of age/risk based investment choices. As Mr. Topp summarizes in the article:

“For participants who want little or no ongoing responsibility for asset allocation decisions, we believe a suite of age-based asset allocation funds is an excellent solution. . . . these products are simple to select and provide participants with diversification, automatic rebalancing, and a glide-path that will de-risk their portfolio over time.

For the participant who wants to take an active role in managing their asset allocation, your responsibility is to provide a core group of funds that will allow a participant to build a well-diversified portfolio that will provide them with growth opportunities regardless of the financial environment.”

There is more worth exploring in this article including global exposure and inflation protection – but I think the most important issue is to edit down the menu to the core funds and make sure there is a path to success for all plan participants, not just the financially sophisticated ones.